Progressive lawmakers in Olympia have been talking about tax reform for years, and the conversation always comes back to the issue of fairness. We constantly hear that the tax code is “regressive,” that low-income families “carry the burden,” and that wealthy residents “don't pay their share.” This selective definition of fairness measures just the percentage of a person’s income that is taxed, while deliberately ignoring the total tax burden funding government – which, in Washington state, is growing at a breakneck pace. However, this progressive framing around fairness allows lawmakers to justify raising taxes on high earners and businesses every legislative session.

In reality, taxpayers in Washington’s highest income brackets pay roughly six times more in state and local taxes than those in the lowest brackets, and businesses alone contribute about half of all tax revenue the state collects.

Look at the tax policies that have been passed under the banner of “reform” over the past decade: the capital gains tax, a long-term care payroll tax, B&O rate increases, a sales tax expansion, the Climate Commitment Act, and now an income tax. Despite all these new taxes, the sales tax remains the dominant revenue source for Washington. By the majority’s own preferred metric, the tax code is no less regressive today than it was a decade ago. The state now collects significantly more money, has not cut sales or property taxes, and is still projecting multi-billion-dollar deficits through the end of the decade.

The deficits continue to grow because spending has increased faster than revenue in nearly every budget cycle since 2013, and there is no structural mechanism in place that requires the legislature to stop. That has to change before Washingtonians and the legislature can have a serious discussion about tax reform.

Washington used to have a spending limit

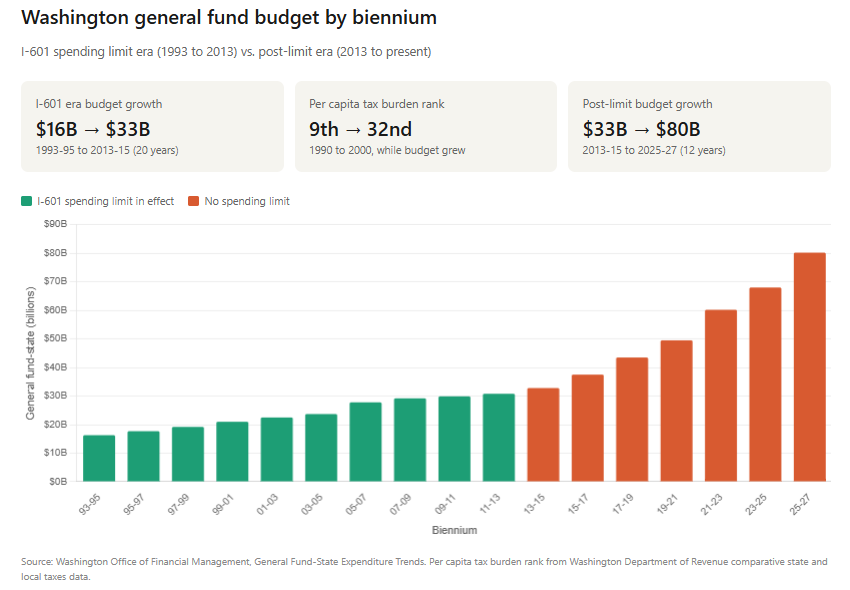

In 1993, voters approved Initiative 601 with 51% of the vote. The measure limited biennial spending to population growth plus inflation and required a two-thirds legislative supermajority to raise taxes. Government would be able to grow as the state grows, but it would not be permitted to outpace the people funding it without either broad legislative consensus or direct voter approval.

According to the Washington Department of Revenue, the spending limit worked. Washington ranked 9th in the country in per capita tax burden in 1990. By 2000, that rank had fallen to 32nd. Washington went from being one of the heaviest tax states in the country to solidly below average in a single decade, while still funding schools, roads, and public safety. Businesses had a different calculus about locating or expanding in Washington than they did 10 years earlier, and residents kept more of their income.

It’s worth noting that the 1990s tech boom unfolded while the spending limit was in place. Any claim that fiscal restraint starves growth is completely detached from Washington's own historical data.

Unsurprisingly, the legislature was not enthusiastic about maintaining the spending cap. They suspended the supermajority requirement during the 2002 budget shortfall, again in 2005, and again in 2010. Each time, a simple majority vote was all it took to increase spending, defeating the entire purpose of having a supermajority requirement in the first place.

Voters pushed back, reaffirming the two-thirds requirement directly through Initiative 960 in 2007, Initiative 1053 in 2010, and Initiative 1185 in 2012 which won 64% of the vote statewide. Referendum 49 in 1998, primarily a car tab and transportation measure, affirmed I-601's spending limits as part of a broader package. That amounts to five voter affirmations over 19 years, but the legislature suspended the supermajority requirement whenever it got in the way of their spending.

The income tax that passed this session follows the same pattern. Voters rejected an income tax 11 times over the past 90 years, but the legislature passed one anyway.

The spending limit ended in February 2013 when the Washington Supreme Court ruled in League of Education Voters v. State that a statutory supermajority requirement for tax increases violated the state constitution's simple majority requirement for passing legislation. The court was clear that if Washingtonians wanted a durable supermajority requirement, it needed to be in the constitution. The legislature never referred that question to voters, and the spending limit was killed.

Spending since I-601 was overturned

General fund spending in 2013-15 was $33.5 billion. The 2025-27 budget comes in at $80.2 billion. Over the same period, cumulative inflation rose roughly 36% and the state's population grew by about 14%. Adjusted for both, real per-capita state spending increased by more than 50%.

The spending growth was not matched by an equivalent increase in revenue, even accounting for the significant tax increases of recent sessions. The state still likely faces a multi-billion-dollar deficit in the 2027-29 biennium. The four-year budget outlook built into the supplemental budget passed this year assumes spending growth well below the historical average, excludes future collective bargaining costs that have been a consistent driver of past deficits, and depends on income tax revenue that has not yet survived a legal challenge or a potential ballot measure.

This is the self-destructive pattern a spending limit disrupts. Without a spending cap, there is nothing to stop the legislature from writing a budget that requires more revenue than currently exists, raising taxes to fund it, committing that revenue to ongoing programs, and then facing the same problem two years later at a higher baseline.

A Constitutional limit would end the cycle

The Supreme Court's guidance in 2013 was clear. A statutory spending limit can always be suspended by a future legislature with a simple majority vote, as the history before 2013 demonstrated over and over again. The only way to make the constraint durable is to put it in the constitution, where changing it requires a two-thirds legislative vote to refer the question to voters and majority voter approval to modify it.

A constitutional spending limit tied to population growth plus inflation would not freeze government at its current size. It would allow the budget to grow, but at a pace connected to the actual growth of the state rather than the growth of the majority caucus' spending appetite.

It would not prevent the legislature from responding to genuine fiscal emergencies, which is what reserve funds exist for. It would not dictate how the state raises revenue or what the tax structure looks like.

What a spending cap would change is the incentive structure. Right now, legislators can spend beyond available revenue, raise taxes to cover the difference, and call that responsible governance and tax reform. A binding spending limit forces a different conversation - one not about where to find more money, but about what the state's existing money should actually pay for.

Real tax reform demands tradeoffs, and those tradeoffs require a fiscal environment where avoiding them is not an option.