Key Findings

- Yakima’s Proposition 1 is a reasonable taxpayer protection policy

- Proposition 1 asks citizens if one extra vote should be needed to raise taxes

- Proposition 1 goes no further than what Yakima voters have already approved at the state level

- Yakima voters have voted for tax limitation policies five times previously

- Historically, a higher vote threshold has required greater discussion about budgeting priorities

- Lawmakers could always allow voters to increase taxes with a simple majority vote

Introduction

On November 5, Yakima voters will decide whether a limit on raising taxes that voters have already approved several times at the state level should also apply to the city of Yakima.

Yakima’s Proposition 1 is similar to a proposal already approved in the city of Spokane and Pierce County. It would increase the number of city councilmembers that must approve to increase the financial burden they place on taxpayers. The change would mean five of the council’s seven members must agree to a tax increase, instead of the current four votes that are needed to raise taxes. The ballot measure says:

Proposition No. 1 concerns an amendment of Article VII, Section 2, of the City of Yakima Charter. The proposed amendment states that, after January 1, 2013, any councilmanic tax may be assessed, levied or increased only by a minimum affirmative vote of five members of the City Council. Should this proposition be approved?

-Yes

-No

Historically, a higher vote threshold has required a greater discussion with citizens about tax increases and budgeting priorities.

Background

The Yakima City Council has the authority to impose a number of taxes, including property, sales, utility, business and excise taxes. Under this proposition, any increase in existing taxes or creation of a new tax would require five votes on the city council or approval by a majority of voters in an election.

City fees would not be subject to the increased tax threshold. The following table explains how the state’s Department of Revenue defines the difference between a tax and a fee.

Tax | Fee | |

Purpose | To raise revenue | To regulate for public welfare or to charge as a user fee |

Application | Applied uniformly in the taxing district | Applied to persons receiving services or for the cost of off-setting the regulatory burden incurred by the fee payer |

Use of funds | General use, for public benefit | Specific use and directly related to the regulatory purpose |

Perhaps the largest regular tax increase most felt in the community is the city’s yearly 1% property tax hike. Under Proposition 1 this tax increase would be subject to the higher vote requirement.

Alternatively, Yakima city councilmembers could send the proposed property tax increase directly to voters for approval.

Supermajorities Are Part of Democracy

Opponents of Proposition 1 argue that supermajority vote requirements are undemocratic. Supermajority requirements, however, are a routine part of all democratic systems. They exist at the federal, state and local levels and are a common feature of democratic governments in other countries.

Washington state’s constitution contains more than 20 supermajority requirements. The most recent was added in 2007, when Democratic Senate Majority Leader Lisa Brown of Spokane and Republican Senator Joseph Zarelli of Ridgefield (Clark County) sent voters Senate Joint Resolution 8206, to require a three-fifths vote of the legislature to spend money from the Budget Stabilization Account. The measure was approved by state voters in 2007. Other examples of supermajority requirements in the state constitution include:

- A two-thirds vote of the legislature to convene a special session of the legislature

- A 60% vote of the legislature or a 60% vote of the people to approve a state lottery

- A two-thirds vote of the legislature to consider a newly-introduced bill within ten days of final adjournment

- A two-thirds vote of the legislature to override a governor’s veto

- A two-thirds vote of the people to relocate the state capitol

Supermajority requirements are also common in Yakima’s charter and city budget rules. For instance, emergency budget ordinances have a higher vote threshold (Charter Ordinance 261-Sections 2 and 6). Many of the city’s own budget rules, including amending the budget, have supermajority requirements.

The U.S. Constitution contains several supermajority vote provisions, including the approval of foreign treaties, overriding a presidential veto, impeachment of a public official and approval of changes to the constitution.

The framers of Yakima’s city charter, the Washington Constitution and the U.S. Constitution did not believe supermajority requirements were unfair or undemocratic. They placed them throughout those documents, believing a higher level of agreement was needed for certain public actions. In fact, legislators have often changed their own rules and adopted higher vote requirements.

By approving a supermajority requirement for tax increases, the people of Yakima would simply be stating a policy preference that they want a higher level of agreement before councilmembers increase the financial burden the city places on citizens.

Local Support for State’s Supermajority Requirement

Citizens of the city of Yakima have a long history of supporting supermajority requirements for tax increases at the state level. By overwhelming majorities, Yakima voters approved the higher threshold needed to raise taxes in 1993, 1998, 2007, 2010 and 2012.

The most recent version, statewide Initiative 1185, passed in Yakima with almost 70% of the vote. The approval rate was high among almost all city and county voting precincts.

2012 – Initiative 1185 – Supermajority Vote Requirement for the Legislature to Raise Taxes

(Yakima County Results)

Yes – 51,701 (69.5%)

No – 22,621 (30.5%)

Supreme Court Ruling: Follow the Local Governments

While the Washington state Supreme Court struck down the state requirement for a two-thirds vote to increase taxes, justices were careful not to dismiss the policy idea altogether.

In the majority ruling, justices said they were not judging the “wisdom” of the policy, but rather how it was put into place. Writing for the majority, Justice Susan Owens said, “should the people and the Legislature still wish to require a super-majority vote for tax legislation, they must do so through constitutional amendment, not through legislation.”

The court essentially endorsed the action that voters in Spokane and Pierce County have taken in adopting a charter amendment requiring a two-thirds vote to raise taxes. Charters serve as a city or county’s constitution.

The Need for More Protection

The effort by lawmakers to raise taxes in the last legislative session shows the need for increased taxpayer protection. Lawmakers spent much of the 2013 session under the voter-approved supermajority requirement, but even when the Supreme Court struck the two-thirds rule, legislators were clearly uneasy about raising general taxes.

Instead, they sought to increase revenues in other ways – by passing costs onto cities and counties and, in turn, giving local governments the ability to raise current tax rates or enact new forms of taxation. Thus, some lawmakers sought to avoid raising statewide taxes themselves, but wanted to make it easier for local officials to increase the tax burden on their citizens. Among the bills legislators considered:

- House Bill 1925 – Allowing a city or county to impose a public safety sales and use tax without voter approval

- House Bill 1954 – Allowing council approval of Motor Vehicle Excise Tax (Car Tab Tax) on vehicle licensing (for certain population areas)

- House Bill 1953 – Allowing transportation districts or county governments to impose their own Motor Vehicle Excise Tax (Car Tab Tax) up to 1% of value of vehicle (for certain population areas)

- House Bill 1959 – Allowing a county council to impose the $40 car tab fee and a Motor Vehicle Excise Tax (Car Tab Tax) of up to 1.5% of value of vehicle (for certain population areas)

- House Bill 1865 – Allowing local “transportation benefit districts” to raise sales taxes without a vote of the people (for certain population areas)

While none of these bills passed in the recent session, some local lawmakers saw the opportunity and began to eagerly anticipate spending more taxpayer money.

Kirkland City Councilman Dave Asher said “if you give us local tax increase options, we will use them.”

Case Studies: City of Spokane and Pierce County

In February, voters in the city of Spokane were the first in Washington to adopt a city supermajority requirement. Six of the seven council members agreed it should be placed on the ballot and a majority of citizens approved the change. The supermajority rule is similar to Yakima’s proposed Proposition 1.

Last fall, concerned about the cost shift onto local governments, the Pierce County Council decided to send a measure to voters requiring a supermajority for new taxes in Pierce County. Like Spokane, it was approved.

Michigan and Colorado’s Requirements

Yakima’s proposed charter change does not go as far as other states’ taxpayer protections. In Michigan, for example, local lawmakers are subject to the Headlee Amendment, which requires voter approval of all tax increases at the state and local level.

In Colorado, voter approval is required of all tax increases before they can become law. Despite the claims of opponents that the requirement would hamper the ability of lawmakers to do their job, voters have shown a willingness to increase their financial burden when they are shown how their hard-earned tax dollars will be spent. In fact, in the 2012 election, 11 Colorado cities approved tax increases to fund various public services.

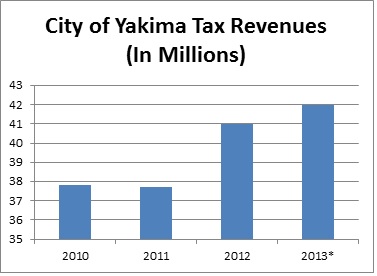

Yakima’s Budget and Tax Revenues

Yakima voters are already generous in the amount of money they give to city government. For instance, last year property tax revenues to the city were anticipated to increase by 4%. City councilmembers also expected to have 19.2% more to spend from the city’s utility tax revenue.

Over the past four years, during an economic downturn that has reduced the median household income of a Yakima Valley citizen to one of the lowest in the state, tax revenue to the city of Yakima has steadily increased, to a total of $42.1 million in 2013 – 11% higher than it was just four years ago.

Conclusion

Proposition 1 asks Yakima voters to adopt a reasonable taxpayer protection policy at the local level, one that they’ve already approved five times at the state level. It does not make increasing taxes impossible; it simply requires lawmakers reach greater consensus before raising the financial burden they place on citizens. “It has forced lawmakers to fully debate the merits and compromise,” the Walla Walla Union-Bulletin said of supermajority requirements. In the absence of consensus on the council, lawmakers could always allow voters to approve tax increases with a simple majority vote.

Proposition 1’s tax limitation policy is the same as the tax limitation measure Spokane voters approved at the city level, and similar to what Pierce County voters adopted at the county level. It also does not go as far as tax limitation requirements currently in force in other states. If they pass this proposed charger change, Yakima voters would clearly frame the city’s budget debate and send a strong message to state legislators that proposals to increase the tax burden should not be shifted on to local taxpayers.

Chris Cargill is the director of the Eastern Washington office and Jason Mercier is the director of the Center for Government Reform at Washington Policy Center, a non-partisan independent policy research organization in Washington state.

Download a PDF of this Policy Brief here.