Seventy-two years ago, America's 12-year Great Depression began with a crash. The bottom fell out of the stock market on October 24, 1929, signaling the start of the longest and deepest economic decline in the nation's history. Now that we are in an economic downturn, everyone wants to know if a crash could ever happen again.

"Black Thursday," as October 24 was called, shook many industries within Washington state. Although the tragedy didn't impact Washington as much as other states, the effects of the depression and various government policies significantly harmed particular sectors.

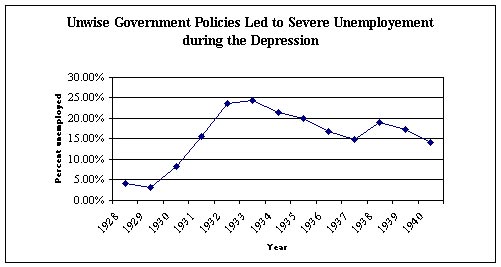

Joblessness in the United States sharply increased after the Federal Reserve-induces crash of 1929. Ballooning government taxes and regulation in the 1930s kept the country mired in economic distress.

By 1932, wheat prices in Washington dropped to .38 cents a bushel from a price of $1.83 per bushel in the early 1920s. The value of Washington farmland and buildings by 1935 had dropped from $920 million to $551 million; while county debt statewide increased 300% and payrolls dropped 36%.

The lumber industry within the state was hit particularly hard by the economic decline. Per capita consumption of lumber in the United States dropped by two-thirds between 1929 and 1932. In that same period, Washington's annual lumber production decreased from 7.3 billion feet to 2.2 billion feet. At least half of those employed by mills were unemployed by the end of 1931.

The policies of the Roosevelt administration didn't do much to help the lumber industry. In 1933, the National Industrial Recovery Act (NIRA) was passed, imposing strict production limits and price controls on individual industries. Before the Act was ruled unconstitutional in 1935, it prohibited building new sawmills and individual operators were only allowed to produce a specific quota. Due to failed federal monitoring, more sawmills were built and total production per firm decreased.

One section of the NIRA greatly expanded big labor's organizing power and made it mandatory for managers to bargain with unions. Today, historians see the solidification of Washington's labor movement as the direct result of implementing New Deal policies in the Pacific Northwest.

Could a Great Depression happen again? Possibly, but it would take a repeat of the bipartisan and devastatingly foolish policies of the 1920s and ' 30s to bring it about.

For the most part, economists now know that the stock market did not cause the 1929 crash. It was itself a symptom of wildly erratic shifts in the nation's money supply. The Federal Reserve System was the primary culprit, having stimulated a boom with dirt-cheap interest rates and easy money in the early ' 20s. By 1929, the central bank had jacked up rates so high that it choked off the boom and forced a reduction in the money supply by one-third between 1929 and 1933.

In 1930, Congress took a recession and turned it into a Great Depression. It raised tariffs so high they virtually closed the borders to imports and exports. It doubled income tax rates in 1932. Franklin Roosevelt, who campaigned on a platform of less government, actually gave America much more. His "New Deal" raised taxes (he once proposed a 99.5 percent tax rate on incomes over $100,000), punished investment and smothered business with rules and red tape.

Like all states, Washington is dependent upon the whims of federal policymakers. And the formula for producing economic depressions remains the same: choking off freedom in the market, crushing incentive with high tax rates and overwhelming businesses with stifling regulations.

The crash of '29 and the subsequent Depression are worth remembering not only because they produced great pain in Washington and elsewhere, but also because as philosopher George Santayana warned, "Those who cannot remember history are condemned to repeat it."

Lawrence W. Reed is director of Mackinac Center for Public Policy in Michigan and an adjunct scholar of Washington Policy Center in Seattle. WPC Researcher Jason Smosna contributed to this commentary.