I recently attended a meeting in Olympia at which former Washington State Department of Transportation Secretary Paula Hammond shared a presentation on the Road Usage Charge Pilot Project. The pilot, spearheaded by the Washington State Transportation Commission, would simulate what it would be like for drivers to pay a tax on every mile they drive.

I took the opportunity to ask Paula about the 18th amendment, which protects gas tax revenue for highway purposes only, and whether a mileage tax would have the same protection. I will get to her response a little later.

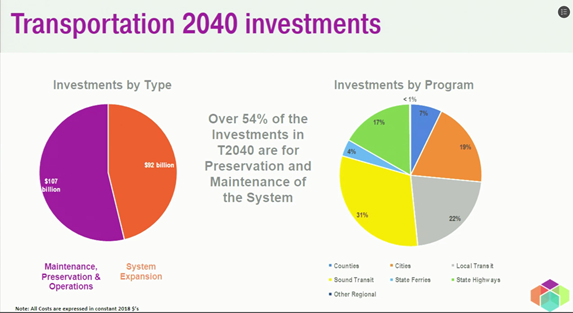

In the way of a little background, according to a recent update by the Puget Sound Regional Council (PSRC), government officials would like to see 53% of investments going to transit, with only 17% of investments going to highways.

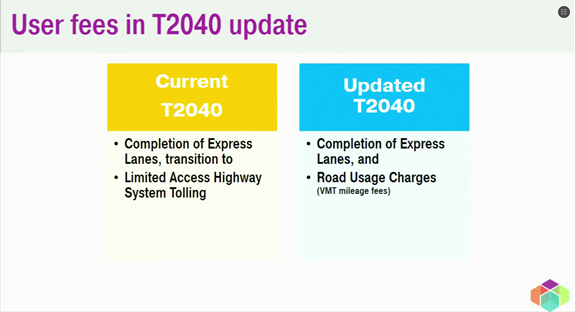

It appears they are counting on the bulk of revenue to come from drivers paying tolls and mileage taxes.

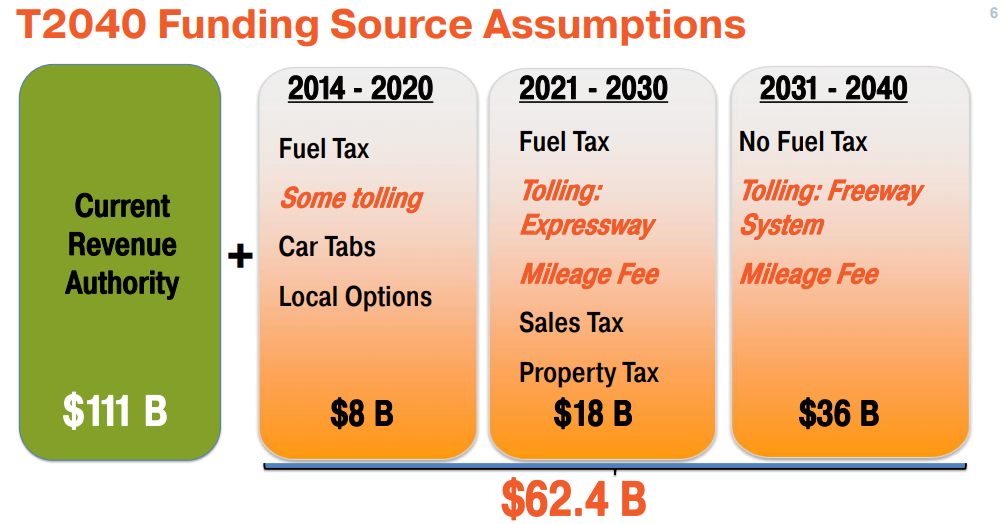

From a 2016 presentation:

To accomplish this vision, the PSRC would like to see the state get away from revenue “silos,” like the 18th amendment, and have more “flexibility in expenditures.”

In the ideal world of government, drivers would pay a mileage tax, and government would get to decide what they think is the most efficient use of those dollars. According to the PSRC, which sits on the Road Usage Charge Steering Committee, it appears they believe the most efficient use of drivers’ money is on public transportation, which carries a fairly steady but very low 4% share of trips in our region, while single and high occupancy vehicles will make up over 80% of trips in the region by 2040.

The reason I asked whether a mileage tax would be protected by the 18th amendment is because that clearly doesn’t seem to be the desire of planners in the Puget Sound.

I did not receive a clear answer to my question – only that that this is a conversation the committee has had but that this is not really a top priority right now. They are more focused on getting the pilot done, and will get into the weeds of things like the 18th amendment later.

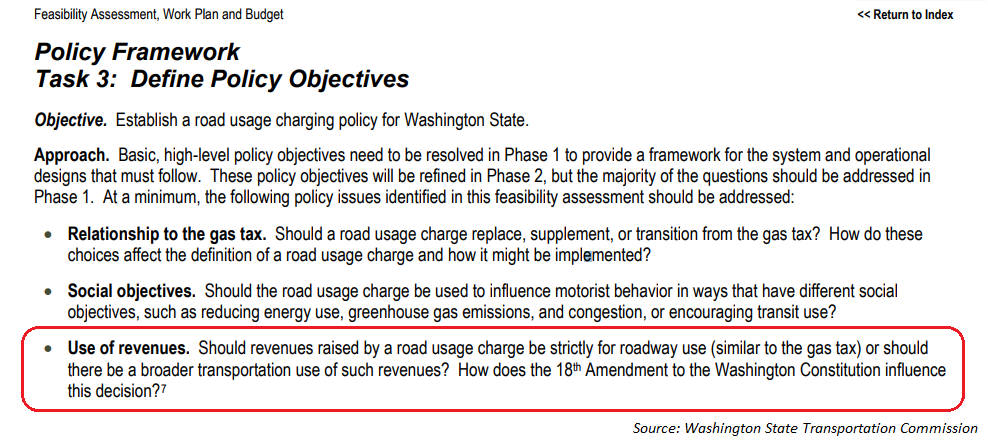

This is echoed by the Commission in a 2013 study, where they list “use of revenues” as an undefined policy objective that should be addressed: “Should revenues raised by a road usage charge be strictly for roadway use (similar to the gas tax) or should there be a broader transportation use of such revenues? How does the 18th Amendment to the Washington Constitution influence this decision?”

While the legislature would have to make a decision about 18th amendment protection, the Road Usage Charge Steering Committee has a tremendous amount of influence and will provide lawmakers with recommendations.

The lack of clarity on the 18th amendment at this point in the project is striking.

It is bad government to first pass a pilot project and promote acceptance (and perhaps passage) of a new tax, and decide how the money should be spent afterward. Instead, public officials should first decide what their principles are that will guide expenditures, what they need money for, how they plan to spend it, and then decide how that money should be raised. This requires a degree of transparency and honesty with taxpayers.

Unfortunately, that is not what we see so far. The 18th amendment, which guides and restricts spending, is treated as an afterthought.

In reality, it is the number one issue surrounding any new funding mechanism that is promoted as a replacement to the gas tax. A funding mechanism that is not protected by the 18th amendment serves an entirely different purpose than the gas tax, and it is disingenuous to claim otherwise.