Sound Transit's bad week could get worse - a new finding

Sound Transit’s terrible, horrible, no good, very bad week could get worse.

Our research revealed that the transit agency has been dishonest with the public, lawmakers, Attorney General, and the Supreme Court about their “obligation” to collect car tab tax overcharges using a repealed 1996 valuation. The agency drafted the incorrect depreciation schedule into statute in 2015, authorizing the agency to collect an additional 0.8% motor vehicle excise tax (MVET) based on this old schedule – even though the agency is using a 1999 valuation.

With no backing from the state Attorney General’s office, which admitted their error and pulled out of presenting at oral argument one hour before the court hearing, Sound Transit’s arguments appeared to fall flat before the Supreme Court justices.

New information

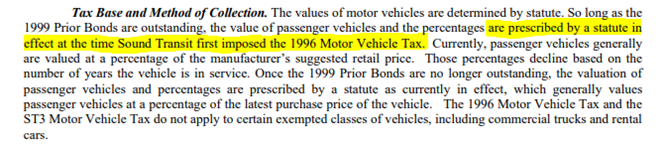

We now suspect the agency’s lawyers/underwriters may have made this same mistake in their bond contract that was issued in 2016 against the Sound Transit 3 sales tax increase and car tab tax of 0.8%. From page 13 of the contract:

The bond contract refers to a valuation that was prescribed by statute in effect at the time Sound Transit first imposed the 1996 Sound Move MVET of 0.3%. The MVET was imposed in 1997, using the 1996 schedule. Sound Transit did not start using the 1999 schedule until after the passage of Referendum 49 in 1998, which triggered the change in July the following year.

In other words, unless there is a legal loophole I’m not aware of, both the 2015 statute and 2016 bond contract regarding the ST3 car tab tax – are wrong. Sound Transit is not using the depreciation schedule either document refers to.

This matters on several fronts:

- Sound Transit lawyer Desmond Brown argued before the Supreme Court that “the depreciation schedule is a necessary and explicit part of our bond contracts.” Apparently it isn’t – because the depreciation schedule referenced in the 2016 bonds is not being used.

- Sound Transit’s former CFO Brian McCartan argued before the Senate Transportation Committee in 2017 that Sound Transit is “contractually obligated to maintain the depreciation schedule while the [1999] bonds are outstanding.” By Sound Transit’s logic, it would then follow that Sound Transit is contractually obligated to maintain the depreciation schedule while the 2016 bonds are outstanding also – except they refer to the wrong depreciation schedule that is, in no way, tied to the MVET the bonds are backed by.

- Sound Transit also argued before the Senate Transportation Committee that they chose to use the “old valuation” for the Sound Transit 3 car tab tax increase so they would not be in the position of imposing two separate valuations on the same piece of property (car). But according to what is written in the 2015 law and in the 2016 bond contract, that is exactly what Sound Transit is doing. The Sound Move car tab tax uses the 1999 valuation, and the Sound Transit 3 car tab tax is under the 1996 valuation.

It is difficult to believe Sound Transit officials, who spend millions in public money on legal counsel, could have made this mistake.

The agency’s argument for the last three years about why they cannot provide relief to the public by simply switching to a new and fair vehicle valuation method is that the law and bondholder contracts are ironclad and dictate that they continue to use the old valuation.

We now know this is not true – either by way of additional dishonesty or simple incompetence on the part of the transit agency.

Sound Transit has no excuse to withhold tax relief, except for one – they don’t want to.